Forget the commentary; the August meeting runs on four numbers.

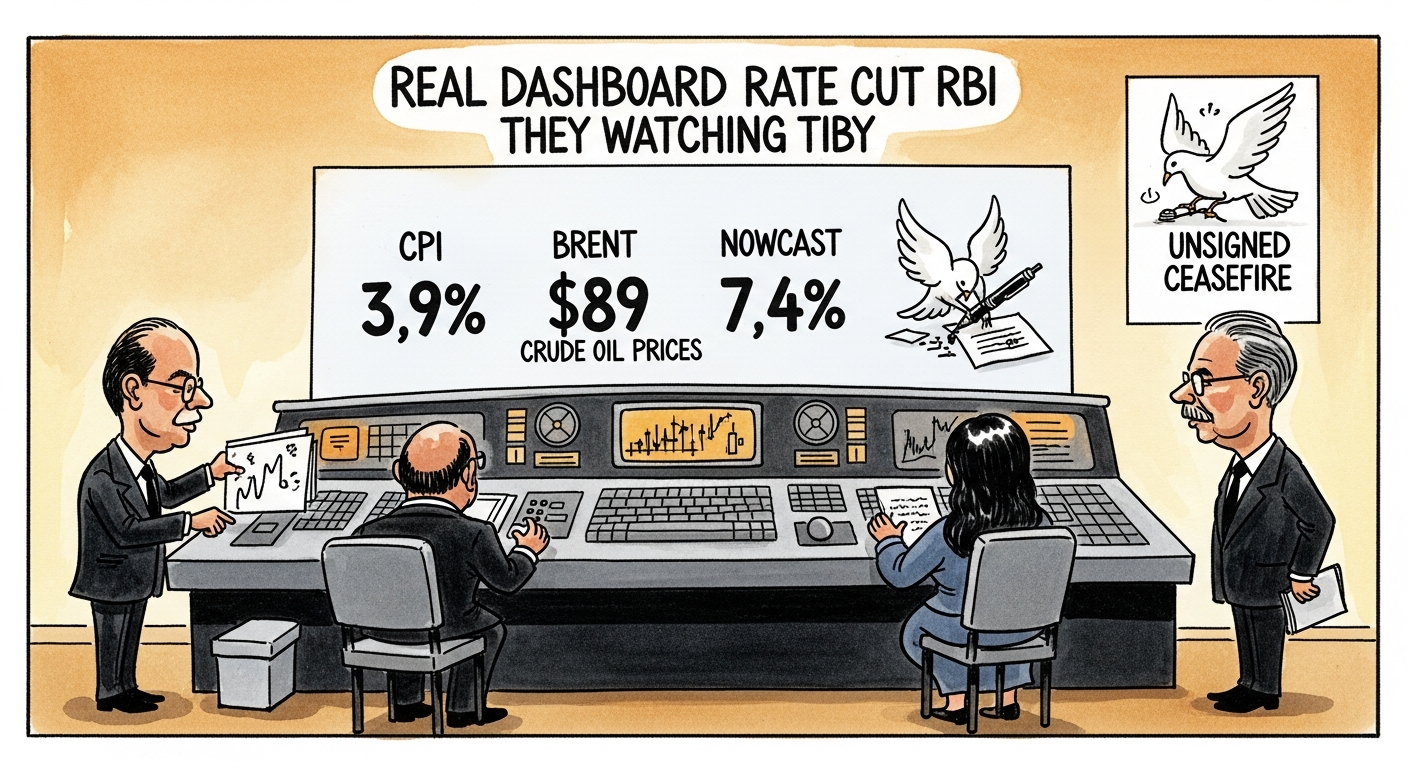

3.9 — July's headline CPI, below the target midpoint four months after crude touched $166. The pass-through that never came is the cycle's quiet achievement, and it hands the doves their opening argument.

89 — Brent's four-week ceiling. Every dollar below 90 rebuilds the current-account cushion and shrinks the war premium in the swaps market, which now prices an August cut at seventy percent.

7.4 — the June-quarter growth nowcast. It kills the recession-insurance case for cutting AND the overheating case for holding; what remains is real rates at their most restrictive since 2019 against a visible disinflation trend.

December — not a number but a date: the Hormuz corridor's mandate renewal. An unsigned ceasefire is the hawks' whole remaining case, and it is not nothing.

The consensus call: a cut framed as insurance, not a cycle. The sentence to read twice in the statement: the first time a UN shipping lane appears as a monetary-policy input. More on the economy desk.