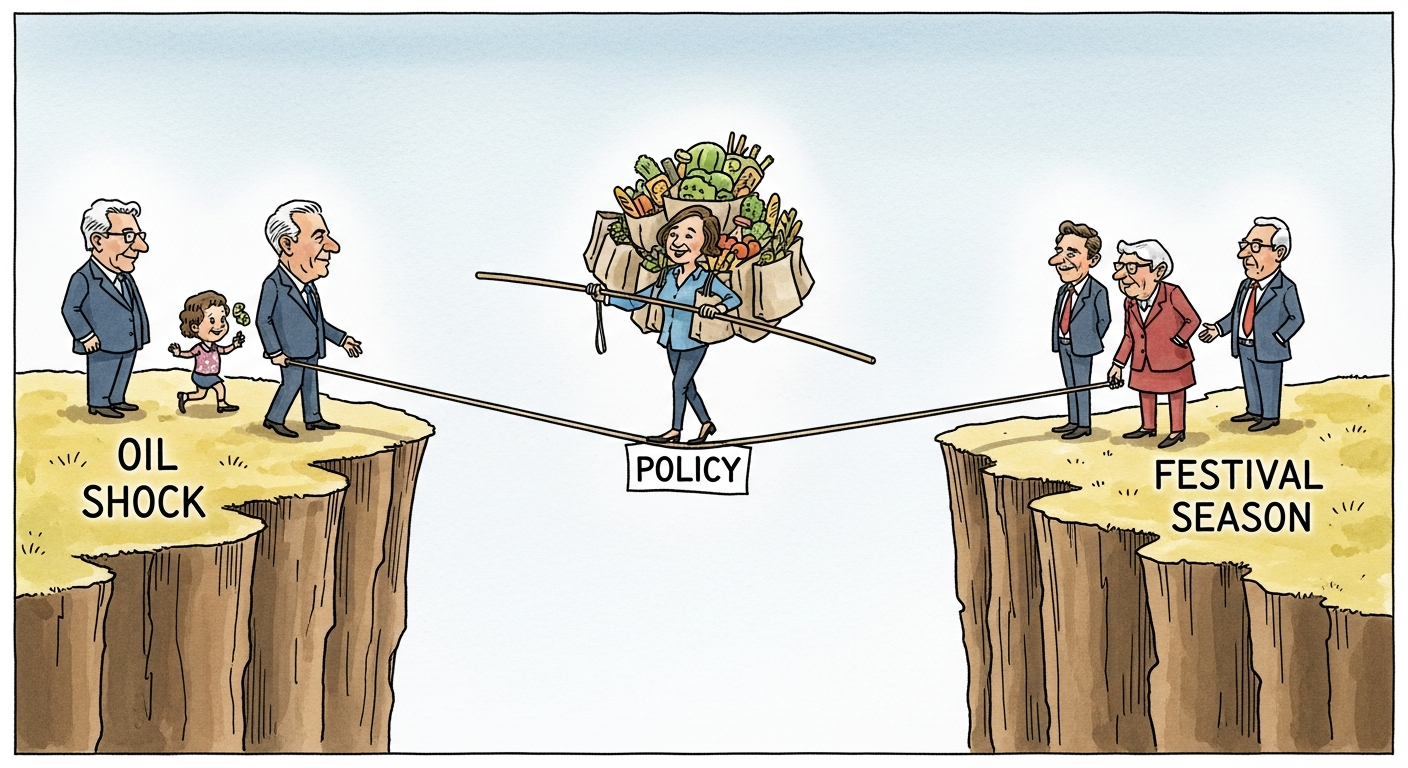

There is a genre of economic achievement that produces no ribbon-cuttings: the number that stays boring through events that should have made it terrifying. July's headline CPI print of 3.9 percent — four months after Dubai crude touched $166 and the country's cooking-gas artery closed — belongs to that genre, and the machinery behind it merits the credit it will never seek.

The counterfactual is recent enough to check. The 2010-13 oil cycle, milder than this spring's, ran Indian inflation to double digits and kept it there; the exchange-rate pass-through of the 2018 episode fed retail prices for a year. This cycle's pass-through was absorbed in a quarter. The differences are institutional, each unglamorous: an inflation-targeting framework old enough to anchor expectations; excise cuts deployed at the spike rather than after the polling; buffer-stock releases and import-window calibration on the food side timed to the monsoon's violence; and a currency defence — $31 billion across two months — that prevented the depreciation-inflation spiral that made 2013 a crisis.

The distributional detail strengthens the story. Rural CPI printed below urban for a third consecutive month — the kharif sowing surplus and the LPG subsidy restructure doing exactly their design work in the consumption basket's most sensitive quintiles.

Risks remain honestly stated: the ceasefire is unsigned, the corridor's December renewal is a live variable, and one violent-delivery monsoon fortnight can put vegetables back in the headlines. Nobody serious declares victory over an index.

But steady prices through an energy war is the macroeconomic equivalent of a bridge that holds in an earthquake — invisible engineering, noticed only in collapse. The bridge held. The engineers were competent. The data keeps saying so, month after boring month.