Networks have thresholds where subsidy stops mattering. ONDC's architects privately set theirs at a crore of daily orders; it crossed this month, and the composition matters more than the count.

Food and mobility seeded the network when the duopolies refused to join. The growth engine now is grocery and general merchandise, on a seller base platforms never built: 1.4 million sellers, seventy percent from beyond the top-twenty cities — businesses whose onboarding economics no marketplace could previously afford.

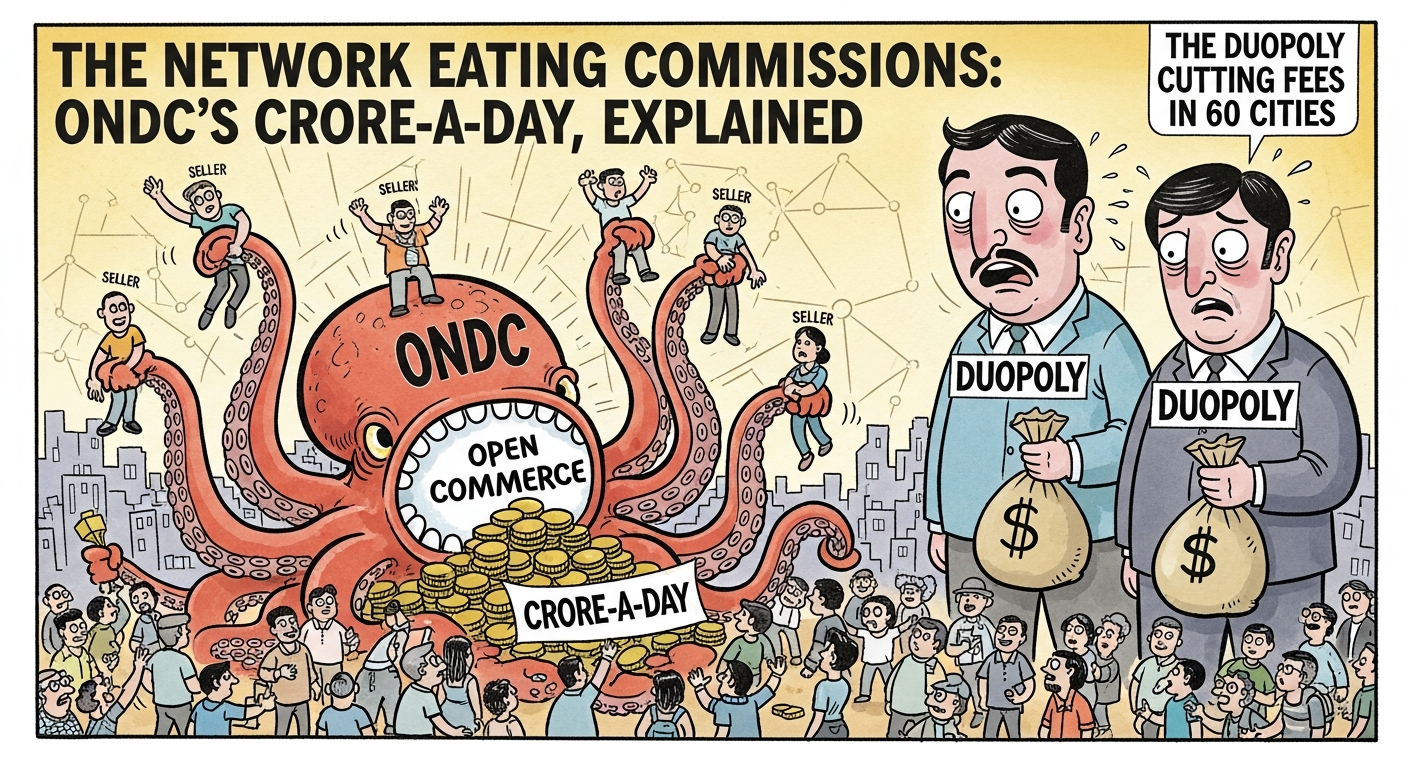

The thesis vindicated: unbundle buyer app from seller app from logistics, let any node transact with any other, and commissions collapse — network averages run at a third of platform-era norms. The clearest tell is defensive: the food-delivery duopoly has cut fees in the sixty cities where ONDC's kitchens run thickest. Contestability was always the point, as with UPI's corridor effect.

Scale's problems arrived on schedule: grievance clocks needed service-level penalties in May; open-network logistics is uneven exactly where growth is fastest.

The pattern is now Indian infrastructure's signature: mocked, then measured, then load-bearing. UPI crossed this same line in 2017. Watch the curve on our tech desk.