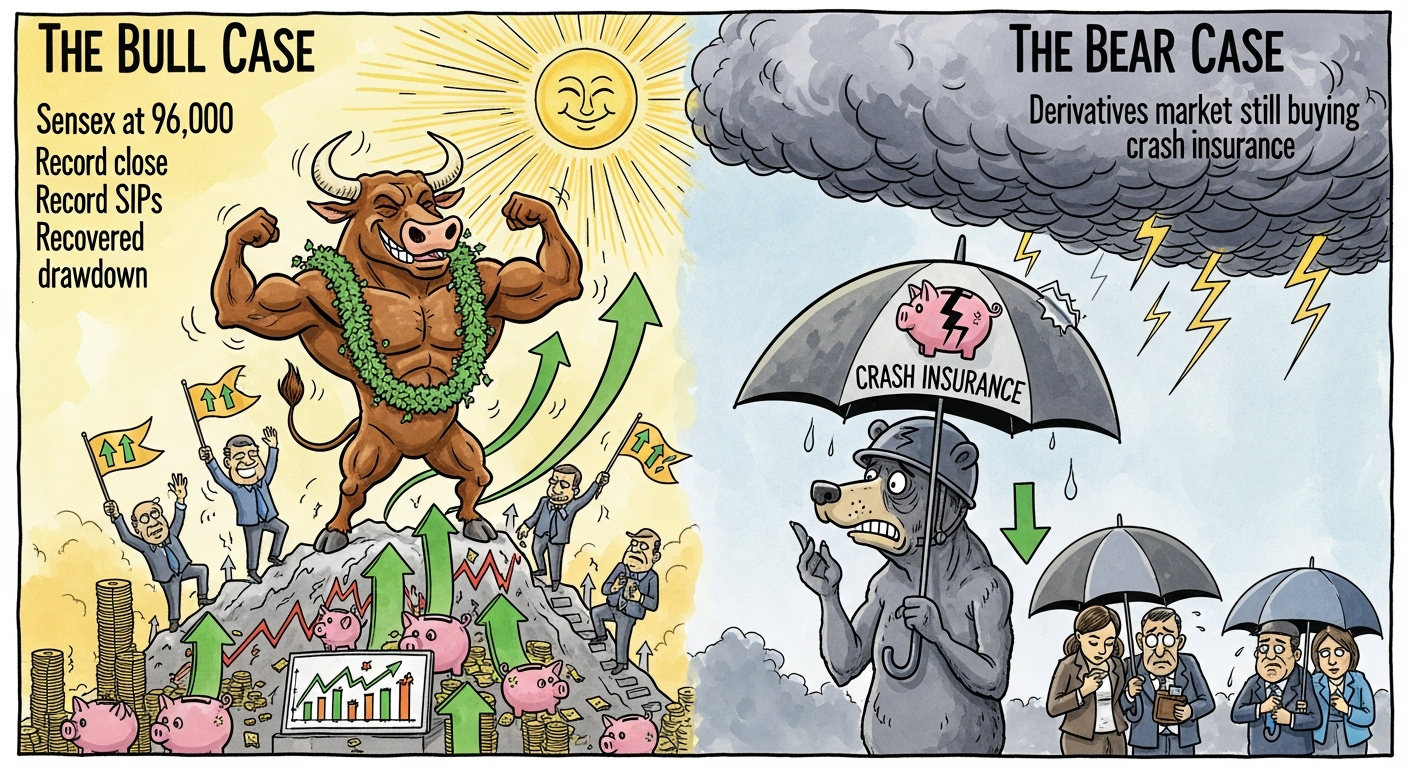

The bull case: the war-quarter drawdown is fully recovered; GST 2.0 hands consumption a September tailwind; the August rate cut would reprice credit; FPIs have bought for seven straight weeks; and SIP inflows above ₹31,000 crore a month mean the marginal buyer is a salary date, not a sentiment. Earnings season opens with a 7.4 percent growth floor under it.

The bear case: India VIX sits two points above pre-war normal and the far-dated options skew still prices a fat left tail — the market enjoying a ceasefire it does not trust. War-risk premia in physical shipping run four times February levels, saying the same thing in cargo language. Valuations lean on a corridor whose mandate renews in December by diplomatic consent.

The tiebreaker is which risk you think is priced: another strait closure (partly) or a durable settlement (not at all). Asymmetry, oddly, favours the boring outcome.

The discipline: the retail bid that absorbed an energy blockade without redeeming is structural, until proven otherwise. Records invite vertigo; flows pay the bills. Daily reads on the economy desk.